Renewable gases to decarbonise the power system

Introduction

There is significant pressure on the electricity industry to decarbonise their power systems as part of the response by many countries to reduce emissions of carbon dioxide. CIGRE is supporting industry in examining the methods to connect renewable energy sources with energy uses as part of this process. There are a number of Study Committees with working groups examining the technical aspects of decarbonisation. Study Committee C5 has contributed with two working groups examining the general issues:

- Working group C5.21 examined the environmental impacts on power systems, using case studies to show the impact of environmental regulations that place prohibitions on thermal generation and environmentally driven schemes that incentivize the development of renewable generation. The working group concluded[1], inter alia, that:

“These policies have contributed to a paradigm shift in how electricity is generated, with a greater focus on environmental sustainability. The successful implementation of these policies greatly depends on the success of power market adaptations to changing fuel mixes.”

- Working group C5.32 is examining the role carbon pricing in wholesale electricity markets. The working group is yet to report but its preliminary findings are that:

- Despite the fact that carbon pricing is one of the most efficient ways to achieve emissions reduction goals, implementing a carbon price that has a significant impact on the electric power sector and resulting GHG emissions is politically very difficult.

The exception is Europe, where a significant carbon price has been enabled, leading to a reduction in fossil fuel generation.

- Impacts on wholesale electricity markets have therefore, with the exception of Europe, been minimal.

As Working Group C5.21 noted the changes to power markets to integrate renewable energy sources as well as to use renewable fuels will be important. A number of SC C5 working groups have examined issues related to the issues with integration of intermittent energy sources into the grids. These focused on how the existing market is changing to manage the intermittency:

- Working groups C5.19 and C5.26 focused on demand response.

- Working group C5.27 examined markets for flexible generation resources

One focus for decarbonisation has been to electrify existing gas loads using renewable electricity sources. This will lead to additional demands being placed on electricity infrastructure, which, everything else being equal, will come at a major cost as:

- Much of the additional costs (in excess of the renewable electricity that will be needed) will be related to ensuring supply continuity by investing in considerable renewable electricity storage – via several key technologies including pumped hydro, batteries and renewable gas storage.

- There is also the critical issue of investment timing. The development of renewable electricity generation and storage infrastructure to meet any increased demand must be in step with new demand. Otherwise, more greenhouse gases will be produced not less, as marginal production will once again draw on fossil fuel generation sources during the transition.

As a result, there is a focus on how to develop and use renewable gases.

There are a number of renewable gases that could be used to decarbonise the natural gas grid. These include hydrogen and two forms of renewable methane:

Hydrogen produced from water and renewable electricity.

Renewable methane sources:

- Biogas, as biomethane (although biogas can be used directly and play other roles). Currently a lot of biomethane is used to generate electricity; and

- Renewable methane – again using water and renewable electricity but reacted with carbon dioxide using direct air capture (DAC) technologies or other green sources of carbon dioxide such as from the production of biomethane from cleaned up biogas streams.

The current focus of Study Committee C5 is on hydrogen and there are two working groups that are examining the market and regulatory aspects, combining or liaising with Study Committee C1 to address planning and economic issues. These working groups are:

- JWG C5/C1.35, is looking at the Integration of hydrogen in electricity markets and sector regulation and is a joint group with Study Committee C1,

- WG C5.36, is looking for certification of the electricity used to produce hydrogen. This WG will also include a SC C1 representative.

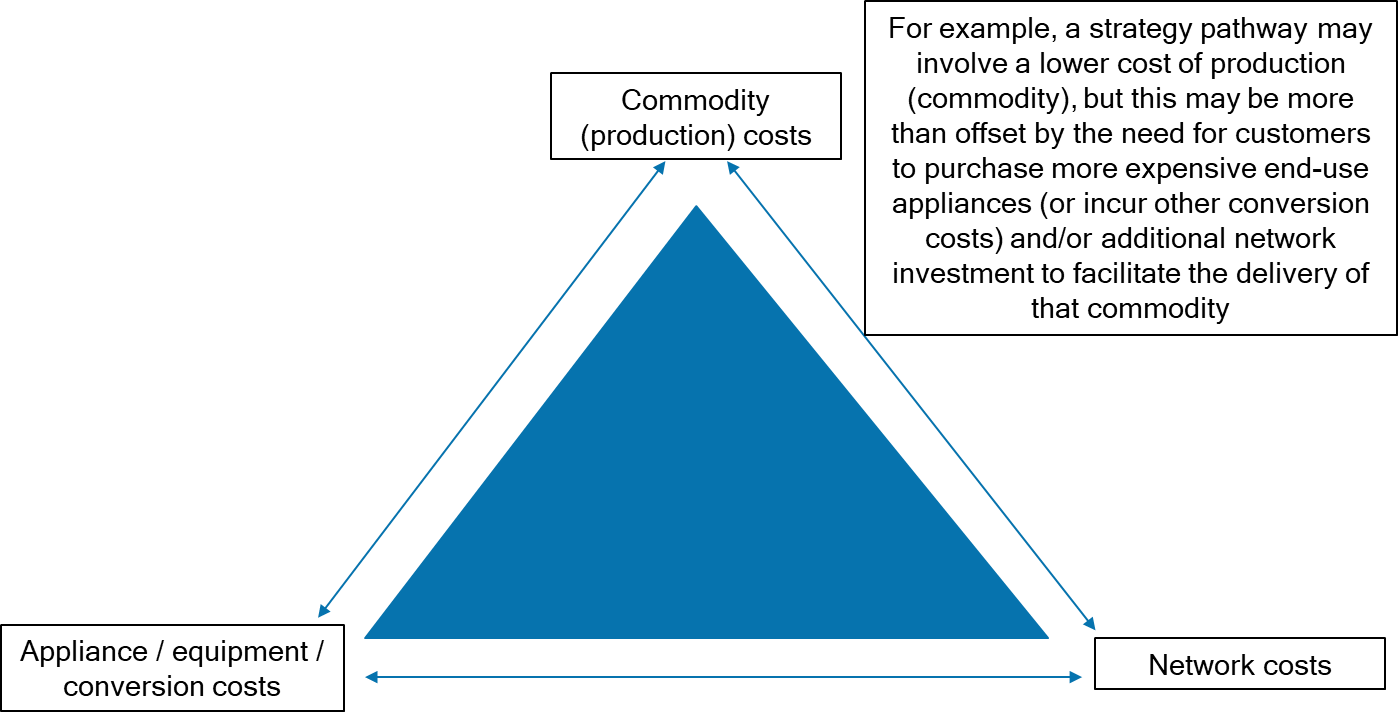

Whichever pathway occurs, it will be important that all of the economic costs are reflected in the decisions that are made by policy makers, see Figure 1.

Figure 1 - Trade-off between the commodity, appliance and network costs of electrification as compared to other renewable gases such as hydrogen and renewable methane - Source: OGW Research Analysis

Integration of hydrogen in electricity markets and sector regulation

Hydrogen is considered a renewable gas that can play a significant role supporting the decarbonising of the power system where electrification is challenging including heat, heavy duty transport and industry. It also has the ability to assist the integration of intermittent, renewable energy. Key uses of hydrogen in the power system are:

- Energy storage. The ability to generate hydrogen from renewable energy and then use the stored hydrogen in a dispatchable generator would allow markets to increase the use of intermittent resources. This capability is being explored for:

- Storage near the intermittent generator as an alternative to batteries for smoothing the output. This can be both for large scale (PV and wind) and small scale (DER PV) generation as well as grid connected generation and remote or isolated uses.

- Storage near loads to allow local smoothing, supporting local reliability and price arbitrage.

- Conversion of generated power for other uses, for example:

- power-to-heat. The hydrogen can be used directly, or blended with other gases as a direct heating source

- power-to-gas. Hydrogen can be used in the manufacture of other gases for direct use. One use already mentioned is to create renewable methane for reticulation and is discussed further below.

- power-to-chemicals, where hydrogen is used as a feedstock.

- An alternative to Battery Electric Vehicles (BEV). Hydrogen Fuel Cell Electric Vehicles (FCEV) are already being trialled and offer an alternative to battery vehicles

It is also worth noting that the transport of hydrogen on land and by sea is already being tried. Like LNG, this offers the ability for countries to import renewable energy rather than fossil fuels.

Currently 95% of the hydrogen produced globally is from natural gas and coal gasification (blue & grey hydrogen). This approach will establish the market for hydrogen starting with grey hydrogen and then reducing the emissions content until green hydrogen (renewable hydrogen) becomes cost competitive in 2030. The regulation, trading systems and market mechanisms must be properly established for this challenge.

Joint Working Group C5/C1.35 will gather information about grid connection to hydrogen technology resources and new initiatives for analysing effect on electricity market such as Capacity Market, Day ahead Market as well as market coupling in Commodity market: Natural Gas price in Spot and Forward Market. In addition, this group will gather hydrogen related information and analyse regulation issues in various countries and continents which currently are established or are planned for the future.

The integration of hydrogen in electricity networks and natural gas pipeline networks needs to consider the economic trade-offs between the alternative approaches. This means that when considering using gas as a means of decarbonisation there is a trade-off between the:

- On-going commodity (production) costs of different decarbonisation pathways.

- Upfront appliance and other switchover costs incurred by customers in switching the fuels or energy sources that power their appliances.

- The network infrastructure costs (both upfront and ongoing) associated with different decarbonisation pathways (e.g., electrification, versus hydrogen, versus renewable methane sources).

Certification of the electricity used to produce hydrogen

For hydrogen to be able to assist in decarbonizing the power system, it is necessary that there are no emissions throughout the fuel production chain, that is that only green hydrogen should be used. As noted above, there may be a transitionary phase where blue hydrogen is used but the emissions should be measured as they are reduced to a low level and, eventually eliminated.

In order for the hydrogen buyer to be sure of the carbon content associated with the fuel, a certification can provide the necessary security to know the fuel's emission footprint. This requirement is very new and there is no standard on how to certify the electrical energy used in this process.

As hydrogen will have domestic and international markets, it is necessary to standardise how to address this issue for different regional conditions and that there are internationally recognised standards.

Working group C5.36 will recommend attributes that are considered to define hydrogen as green and will also structure the parameters that need to be certified so that it is possible to verify if hydrogen is green or if it has a greenhouse gas emission content. This working group, while not its primary focus, may also develop standards for the certification of all electricity sources.

[1] CIGRE Technical Brochure 710 “Impacts of Environmental Policy on Power Markets”, 2017: https://e-cigre.org/publication/710-impacts-of-environmental-policy-on-power-markets